The US check routing number is an essential component of the banking system, playing a critical role in ensuring accurate and efficient processing of financial transactions. Whether you're setting up direct deposits, making payments, or transferring money between accounts, understanding how the routing number works is crucial. In this comprehensive guide, we will delve into everything you need to know about the US check routing number, from its purpose and structure to how to find it on your checks.

For individuals and businesses alike, the US check routing number is a key identifier within the banking infrastructure. It acts as a unique code that helps banks and financial institutions distinguish one another, facilitating the seamless movement of funds across the network. With the rise of digital banking and online transactions, knowing your routing number has never been more important. This guide aims to demystify the US check routing number, offering insights into its significance and practical applications.

As the financial landscape continues to evolve, staying informed about elements like the US check routing number can empower you to make smarter financial decisions. Whether you're a seasoned banking professional or a curious consumer, this guide is designed to provide valuable information and answer common questions related to routing numbers. Let's explore the intricacies of the US check routing number and uncover the vital role it plays in the world of finance.

Table of Contents

- What is a US Check Routing Number?

- History and Evolution of Routing Numbers

- Importance of Routing Numbers in Banking

- How to Find Your Routing Number?

- Understanding the Structure of Routing Numbers

- Differences Between Routing Numbers and Account Numbers

- Routing Numbers in Digital Banking

- Common Misconceptions About Routing Numbers

- How Do Routing Numbers Affect International Transactions?

- Security Aspects of Routing Numbers

- How Are Routing Numbers Assigned?

- Frequently Asked Questions

- Conclusion

What is a US Check Routing Number?

A US check routing number, also known as an ABA routing number or routing transit number (RTN), is a nine-digit numerical code used to identify a specific financial institution within the United States. These numbers are used by banks to process checks and electronic transactions such as direct deposits and wire transfers. Each financial institution is assigned its own unique routing number, which allows for accurate identification and processing of financial transactions.

The concept of the routing number was developed by the American Bankers Association (ABA) in 1910 as a way to streamline the process of check clearing. Since then, routing numbers have become an integral part of the banking system, facilitating the efficient processing of millions of transactions daily. The routing number ensures that funds are accurately directed to the correct financial institution without errors or delays.

The nine-digit format of the routing number is not arbitrary. Each digit or group of digits within the number has a specific meaning, indicating the Federal Reserve district, the bank's unique identifier, and a check digit used for validation purposes. Understanding this structure is important for anyone handling financial transactions, as it helps ensure accuracy and prevent errors.

History and Evolution of Routing Numbers

The history of routing numbers dates back over a century, with their inception rooted in the need for a systematic approach to check clearing. In the early 20th century, as the number of banks and financial transactions grew, the American Bankers Association (ABA) recognized the necessity for a standardized system to process checks across various institutions efficiently. The ABA routing number was introduced in 1910, marking a significant milestone in the evolution of banking practices.

Initially, routing numbers were used solely for processing paper checks. However, as technology advanced and digital banking emerged, the role of routing numbers expanded to include electronic transactions. This evolution was driven by the need for faster and more secure processing of payments, leading to the development of automated clearinghouse (ACH) systems and wire transfers that rely on routing numbers to ensure the smooth transfer of funds.

Over the years, the routing number system has undergone several updates and modifications to accommodate the changing landscape of banking and finance. Today, routing numbers are used not only for check processing but also for various electronic payment methods, highlighting their continued importance in the financial ecosystem.

Importance of Routing Numbers in Banking

Routing numbers serve as a foundational element in the banking industry, playing a crucial role in ensuring the accurate and efficient processing of financial transactions. They act as unique identifiers for banks and financial institutions, allowing for seamless communication and transfer of funds within the banking network. Here are some key reasons why routing numbers are important in banking:

- Accurate Identification: Routing numbers help identify the specific bank or financial institution involved in a transaction, ensuring that funds are directed to the correct location.

- Efficiency: By standardizing the process of identifying banks, routing numbers streamline the processing of checks and electronic payments, reducing the likelihood of errors and delays.

- Security: Routing numbers play a role in verifying the legitimacy of financial institutions, helping to prevent fraudulent activities and unauthorized transactions.

- Facilitating Electronic Transactions: In the digital age, routing numbers are essential for processing ACH transactions, direct deposits, and wire transfers, enabling quick and secure movement of funds between accounts.

Without routing numbers, the banking system would be prone to inefficiencies, errors, and security risks, making it challenging to process transactions accurately and promptly. As such, routing numbers are indispensable to the functioning of the modern financial system.

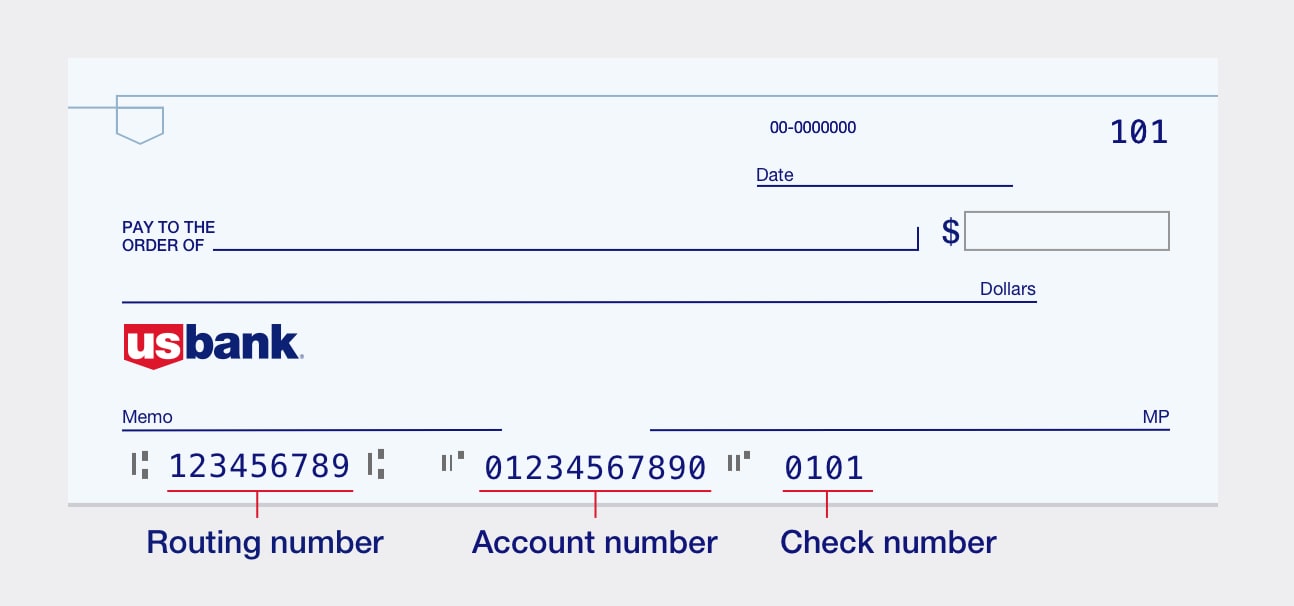

How to Find Your Routing Number?

Finding your routing number is a straightforward process, and there are several methods you can use to locate it. Here are some common ways to find your routing number:

- Check Your Check: The easiest way to find your routing number is to look at the bottom of one of your checks. The routing number is typically the first set of nine digits printed on the left side, followed by your account number and the check number.

- Bank's Website: Many banks provide routing numbers on their official websites. You can visit your bank's website and navigate to the section containing information about routing numbers or contact customer service for assistance.

- Mobile Banking App: If you use a mobile banking app, you can often find your routing number within the app's account information section. This feature is convenient for people who prefer managing their finances digitally.

- Bank Statements: Your monthly bank statements may also include your routing number, usually listed along with your account number.

If you're unable to locate your routing number using these methods, you can always contact your bank's customer service for assistance. It's important to ensure you have the correct routing number, especially when setting up direct deposits or making electronic payments, to avoid any transactional errors.

Understanding the Structure of Routing Numbers

The structure of a routing number is designed to provide specific information about the financial institution it represents. A standard routing number is composed of nine digits, each serving a distinct purpose. Here's a breakdown of what each part of the routing number indicates:

- Federal Reserve Routing Symbol: The first two digits identify the Federal Reserve district in which the bank is located. There are 12 Federal Reserve districts, each represented by a unique code.

- Institution Identifier: The next four digits are the institution identifier, which is unique to each bank. This part of the routing number distinguishes one bank from another within the same Federal Reserve district.

- Check Digit: The final digit is the check digit, used to validate the routing number. It helps ensure the number is accurate and reduces the risk of errors during processing.

Understanding the structure of routing numbers can help you verify their accuracy and prevent potential issues when processing financial transactions. It's crucial to use the correct routing number for your bank to ensure funds are directed to the right institution.

Differences Between Routing Numbers and Account Numbers

Routing numbers and account numbers are both essential elements in the banking system, but they serve different purposes. Understanding the differences between these two types of numbers is important for anyone managing financial transactions:

- Routing Number: As mentioned earlier, a routing number is a nine-digit code used to identify a specific financial institution. It directs transactions to the correct bank, ensuring that funds are accurately processed and routed to the intended recipient.

- Account Number: An account number is a unique identifier assigned to each account holder within a bank. It specifies the exact account to which funds should be credited or debited. Account numbers vary in length and can be anywhere from 8 to 12 digits long, depending on the financial institution.

In summary, while the routing number identifies the bank, the account number identifies the individual account within that bank. Together, these numbers allow for the precise and secure processing of financial transactions, whether they're checks, electronic payments, or wire transfers.

Routing Numbers in Digital Banking

In today's digital age, routing numbers are more important than ever, playing a vital role in the seamless processing of electronic transactions. As banking increasingly moves online, the use of digital payment methods such as ACH transfers, direct deposits, and online bill payments has become more prevalent. Routing numbers are essential for these digital banking processes, ensuring that funds are accurately and securely transferred between accounts.

One of the key benefits of digital banking is the convenience it offers to consumers, allowing them to manage their finances from the comfort of their homes or on the go. Routing numbers are crucial in this context, enabling quick and efficient processing of transactions without the need for physical checks. They also help reduce the risk of errors and fraud, as each transaction is linked to a specific bank and account, providing an additional layer of security.

As digital banking continues to evolve, routing numbers will remain an integral part of the financial ecosystem, facilitating the secure and efficient movement of funds in an increasingly connected world.

Common Misconceptions About Routing Numbers

Despite their importance, routing numbers are often misunderstood, leading to several common misconceptions. Here are some of the most prevalent myths about routing numbers and the truth behind them:

- All Routing Numbers Are the Same: This is a common misconception; each bank or financial institution has its own unique routing number, which distinguishes it from others.

- Routing Numbers Are Only for Checks: While routing numbers were originally created for check processing, they've since expanded to include various electronic transactions, such as direct deposits and wire transfers.

- Routing Numbers Change Frequently: In reality, routing numbers usually remain the same unless a bank undergoes a significant change, such as a merger or acquisition.

- You Only Need a Routing Number for International Transactions: Routing numbers are primarily used for domestic transactions; international transfers typically require a SWIFT code or IBAN.

Understanding these misconceptions can help you better navigate the banking system and avoid potential issues when managing your finances.

How Do Routing Numbers Affect International Transactions?

Routing numbers play a limited role in international transactions, as they are primarily used for domestic banking within the United States. When transferring funds internationally, other identifiers, such as SWIFT codes or International Bank Account Numbers (IBANs), are typically required. These codes ensure that funds are accurately routed to the correct financial institution in another country.

However, routing numbers can still be relevant in certain cross-border transactions, particularly when dealing with US-based accounts or banks that have international branches. In these cases, routing numbers may be used in conjunction with other international identifiers to facilitate the transfer of funds.

It's important to understand the specific requirements for international transactions and ensure that you have all the necessary information, including routing numbers, SWIFT codes, and IBANs, to avoid delays or errors when transferring funds across borders.

Security Aspects of Routing Numbers

While routing numbers are essential for processing financial transactions, they also play a role in ensuring the security of the banking system. Here are some of the key security aspects of routing numbers:

- Verification: Routing numbers help verify the legitimacy of financial institutions, reducing the risk of fraudulent activities and unauthorized transactions.

- Check Digit: The check digit in a routing number is used to validate the accuracy of the number, ensuring that it is entered correctly and reducing the risk of errors during processing.

- Transaction Security: Routing numbers, in conjunction with account numbers, provide an additional layer of security by linking each transaction to a specific bank and account.

While routing numbers are not confidential information, it's still essential to handle them with care and ensure that they are used correctly to avoid potential security risks. By understanding the security aspects of routing numbers, you can better protect your finances and ensure the safe processing of transactions.

How Are Routing Numbers Assigned?

The assignment of routing numbers is a carefully regulated process managed by the American Bankers Association (ABA) in coordination with the Federal Reserve. When a new bank or financial institution is established, it must apply for a routing number through the appropriate channels. Here are the key steps involved in the assignment of routing numbers:

- Application: The bank submits an application to the ABA, providing necessary information about the institution, including its location and structure.

- Approval: The ABA reviews the application and, upon approval, assigns a unique routing number to the bank.

- Publication: Once assigned, the routing number is published and made available to other financial institutions and entities involved in the processing of transactions.

The process of assigning routing numbers ensures that each financial institution is uniquely identified within the banking network, facilitating accurate and efficient processing of transactions.

Frequently Asked Questions

What is the purpose of a routing number?

The purpose of a routing number is to uniquely identify a financial institution within the United States, facilitating accurate and efficient processing of financial transactions such as check clearing, direct deposits, and wire transfers.

Can a bank have more than one routing number?

Yes, a bank can have multiple routing numbers, particularly if it operates in multiple regions or has merged with other institutions. Each routing number is used for specific types of transactions or branches.

How do I find the routing number for my bank?

You can find your bank's routing number on your checks, your bank's website, your mobile banking app, or by contacting customer service. It's typically the first nine-digit number printed on the bottom left of a check.

Is my routing number the same as my account number?

No, your routing number and account number are different. The routing number identifies your bank, while the account number identifies your individual account within that bank.

Do routing numbers change?

Routing numbers rarely change unless there is a significant event, such as a bank merger or acquisition. It's important to verify your routing number periodically, especially if you're aware of changes within your bank.

Are routing numbers used in international transactions?

Routing numbers are primarily used for domestic transactions within the United States. For international transactions, SWIFT codes or IBANs are typically required to accurately route funds to the correct bank in another country.

Conclusion

The US check routing number is a fundamental component of the banking system, ensuring the accurate and efficient processing of financial transactions. By understanding the purpose, structure, and importance of routing numbers, you can better navigate the complexities of the financial world and manage your transactions with confidence. Whether you're setting up direct deposits, making electronic payments, or transferring funds, knowing your routing number and how to use it is crucial for avoiding errors and ensuring the security of your financial activities.

As the financial landscape continues to evolve, staying informed about elements like the US check routing number can empower you to make smarter financial decisions. We hope this guide has provided valuable insights into the world of routing numbers and their vital role in the banking ecosystem.

For further information, you can visit Federal Reserve's official website to learn more about the role of routing numbers in the US banking system.

You Might Also Like

Meek Mill Place Of Birth: A Deep Dive Into His RootsMastering Instagram: How To Turn Off Thread Notifications And Optimize Your Experience

Exploring The Majestic Peaks: Denver City Height And Its Impact

Olivia Rodrigo Phone Number: Facts And Information

The First James Bond Character: A Timeless Legacy In Cinematic History

Article Recommendations

- All About Bts Rm The Multitalented Leader Of The Global Sensation

- Latest Kannada Movies 2022 Movierulz Downloads

- Latest Telugu Movies 2023 Download Now